By: Darren W. King | Wealth Management

Source: Bloomberg, Inc.

Key Takeaways:

Equity Strategy

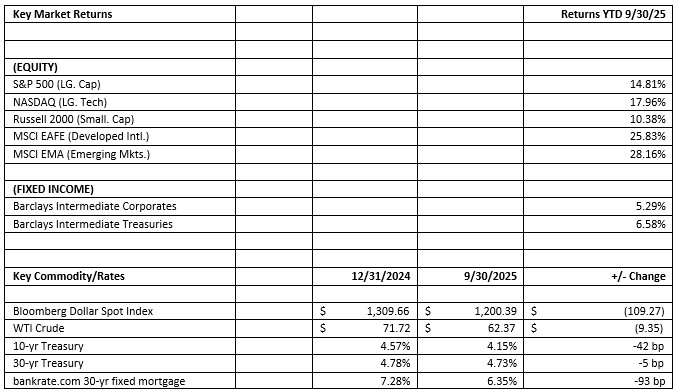

Equity markets have exhaled a huge sigh of relief as the Trump administration’s “shock and awe” tariff policy announced in April have been negotiated to levels in the 15% range. Buy the dip investors have rallied equity markets in the US back to new market highs following resilient corporate earnings, strong AI server spend, expectations for further Fed rate cuts, and extension of corporate and individual tax rates in Trump’s “big beautiful bill”. We continue to favor cyclical sectors over defensive stocks and advise the continued diversification into a larger international allocation. We continue to focus on equities that benefit from AI technological advances, continued deregulation within financials, and value in the recent health care selloff as the Trump administration is walking back 100% tariffs on prescription drugs. We continue to deemphasize consumer sectors with the expected continued pullback in retail spending levels.

Fixed Income Strategy

We are taking a wait and see approach to further bond purchases after the swift movement down in yields, especially on the short end of the yield curve. We see the possibility for yields to move higher, especially considering the recent pickup in consumer spending and GDP growth in the third quarter after weak numbers at the beginning of the year. If the economy falters with tariff pressure and a cost weary consumer; the Fed has ample room to move rates lower from current restrictive Fed fund levels at 4.00%, to a level closer to the current 2.9% inflation rate. Bond allocations would provide a hedge to any equity market weakness should a slowing economy unfold.

Click here to read the entire Q3 2025 Market Review.

Non-Deposit Investment Services are not insured by FDIC or any government agency and are not bank guaranteed. They are not deposits and may lose value.