By: Darren W. King | Wealth Management

Source: Bloomberg, Inc.

Key Takeaways:

Equity Strategy

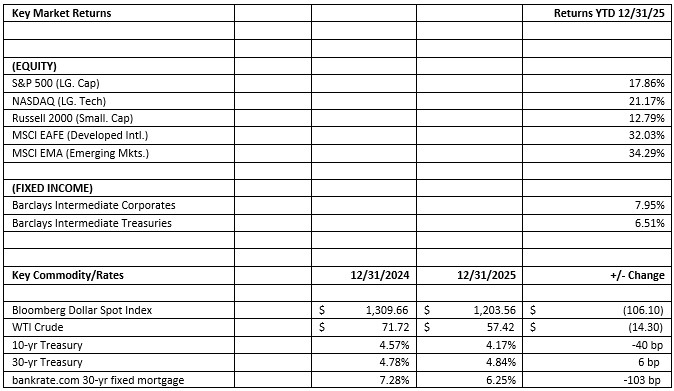

Forward looking, “Magnificent 7” earnings are estimated to grow 22.7% in 2026 with all other S&P 500 constituents expected to grow earnings by 12.5%. The backdrop for equities in 2026 remains supportive for continued gains. Two of the limiting factors for equity returns; rising rates and slowing growth appear to be of limited concern at the present. Corporate tax cuts, accelerated deprecation incentives for capital expenditures, continued AI server spend, and historically high profit margins should drive further gains despite slightly elevated equity valuation levels domestically. We continue to favor cyclical sectors over defensive stocks and advise the continued diversification into a larger international allocation. We continue to focus on equities that benefit from AI technological advances, continued deregulation within financials, and value in the health care sector as Obamacare subsidies have been extended despite earlier worst-case fears.

Fixed Income Strategy

Within the fixed income markets, interest rate, fed policy, and market traders see two more twenty-five basis point interest rate cuts in 2026 and 2027 and a neutral fed funds rate around 3% in the longer-term. We are taking a wait and see approach to further bond purchases after the swift movement down in yields, especially on the short end of the yield curve. With bond maturities and reinvestment, we are extending duration and buying longer-dated maturities.

Click here to read the entire Q4 2025 Market Review.

Non-Deposit Investment Services are not insured by FDIC or any government agency and are not bank guaranteed. They are not deposits and may lose value.